- For those who don’t start fascinated about taxes by January, you are already behind. Planning now saves you time later.

- Tax planning as a freelancer seems daunting until you begin doing it. It is simple to procrastinate, but once you begin tax planning, life will turn out to be easier and in the long run.

- Remember about deductibles! That is probably the most common thing freelancers don’t do, any business expenses are tax deductible.

No proactive fascinated about taxes

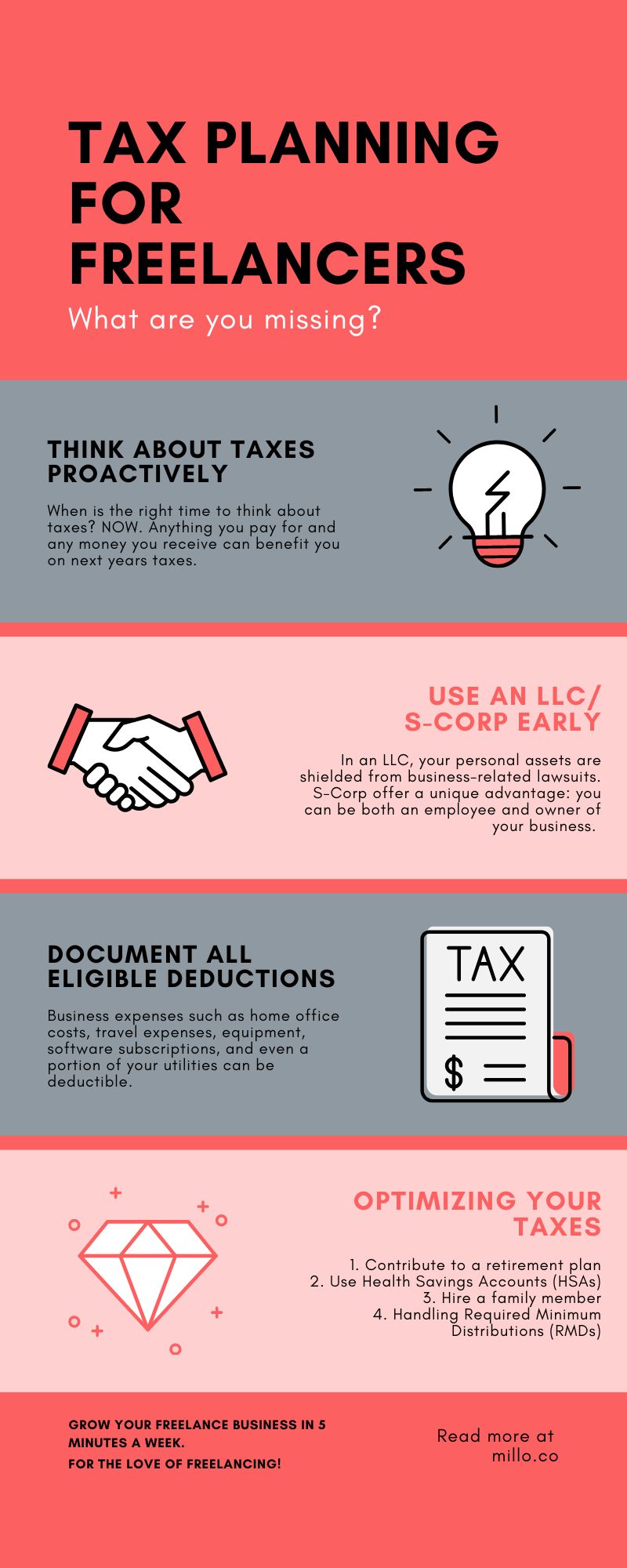

Remember, you’re essentially a small business owner. Freelancers often make the error of taking their taxes as an afterthought, only considering them when tax season approaches. This reactive approach can result in missed opportunities for tax deductions and savings.

Proactive tax planning for freelancers or anyone really involves regular reviews of income, expenses, and potential deductions all year long. This ongoing process lets you discover tax savings opportunities, make crucial adjustments and avoid unwanted surprises within the upcoming tax season. It is crucial to seek the advice of a tax advisor who can show you how to make decisions and supply advice tailored to your specific situation.

As a general rule, to guard yourself, put aside 25-30% of your income for taxes. It will show you how to avoid the dreaded pain of hundreds of dollars in tax season.

Not using an LLC/S-Corp initially

Many freelancers run a sole proprietorship, not realizing that changing the structure of their business can bring significant tax advantages. By operating as an LLC (Limited Liability Company) or S-Corp, you may provide legal protection and tax advantages.

In an LLC, your personal assets are shielded from business-related lawsuits. On the tax side, an LLC provides flexibility as profits and losses can go directly to private income without incurring corporate taxes.

S-Corps, then again, offers a novel advantage: you may be each an worker and the owner of your company. This permits them to be paid a “reasonable wage” and to gather additional income in the shape of a distribution to which they are usually not subject self-employment taxpotentially saving hundreds a yr.

Failure to document all qualifying deductions

Freelancers often overlook beneficial deductions. Business expenses resembling home office costs, travel costs, equipment, software subscriptions and even some utility costs are deductible. It is rather essential to maintain detailed records of all your business expenses all year long.

Do not forget that accurate documentation is crucial. The IRS requires proof of all expenses reported as deductions. So keep your receipts, invoices and bank statements. Think about using a mobile app or cloud-based system to trace expenses and store data digitally.

Tax optimization

Tax optimization involves the use of legal strategies to scale back the tax liability. Listed below are some tax planning strategies freelancers can consider:

1. Contribute to a retirement plan: Self-employed people can contribute to a Simplified Employees’ Retirement (SEP) IRA or Solo 401(k) plan.. These contributions are tax deductible and the funds grow tax free until retirement.

2. Use Health Savings Accounts (HSAs)A: If you might have a high deductible health plan, you may contribute to the HSA. Contributions are tax deductible and payments of qualifying healthcare expenses are tax free.

3. Hire a member of the familyA: If you might have children or other dependents, consider hiring them. You possibly can deduct their salary as a business expense they usually could also be in a lower tax bracket.

4. Support for Required Minimum Distributions (RMD)

If you might have contributed to retirement accounts resembling a 401(k) or IRA, you will have to begin taking RMDs while you reach age 72. RMDs are calculated based on life expectancy and account balance. Failure to gather an RMD can lead to a hefty penalty – 50% of the quantity it’s best to have withdrawn.

When planning an RMD, consider the next strategies:

- Consider a Roth Conversion: If your traditional IRA or 401(k) funds are converted to a Roth IRA, you may avoid the RMD because Roth IRAs would not have this requirement. Remember, nonetheless, that you just will probably be responsible for tax on the converted amount.

- Qualified Charity Distributions (QCD): For those who are inclined to do charity, you may make a QCD from your IRA account. This distribution goes on to the charity of your alternative, counts towards your RMD and will not be included in your taxable income.

- Strategic Withdrawals: For those who retire before your RMD age, consider strategically withdrawing from your retirement accounts to attenuate the RMD impact on your tax bracket in a while.

You’re employed hard for your money, keep it

Navigating the tax landscape as a freelancer may be difficult, but proactive tax planning can show you how to minimize your tax liability and maximize your earnings. Frequently reviewing income and expenses, operating inside the correct business structure, accurately documenting deductions, optimizing taxes, and planning RMD are key strategies.

All the time seek the advice of your tax advisor to be certain you make the most effective decisions for your unique situation. Proactive tax planning is not only about saving money – it’s about constructing a solid financial future.

Turn out to be even more financially sound with our free rate calculator for freelancers.

Keep the conversation going…

Over 10,000 of us are chatting each day in our free Facebook group and we would like to see you there. Join us!