VIX hit a recent yearly low. S&P 500 hit a recent yearly high. Playing for a pullback by buying puts on SPY has never been cheaper over the past 12 months.

We prefer to employ a multi-faceted approach to trade idea generation at POWR Options. Combining fundamental, technical, and implied volatility (IV) evaluation to search out an edge.

A quick walk through of the method is highlighted our most up-to-date evaluation of the S&P 500 below. We’ll use each SPX and SPY interchangeably within the discussion since many traders likely trade SPY versus SPX.

Valuations

All the time prefer Price/Sales versus the more widely followed Price/Earnings (P/E) ratio since earnings might be more easily gamed by stock buybacks and accounting tricks. Price/Sales is a cleaner number.

The recent run-up within the SPX wasn’t based on torrid earnings or revenue growth but was simply more of a multiple expansion.

In terms of revenues, analysts have decreased their estimates through the upcoming quarter. As of Friday, the S&P 500 is predicted to report (year-over-year) revenue growth of three.2%, in comparison with the expectations for revenue growth of three.9% on September 30. So, slowing growth on the horizon.

The present Price/Sales (P/S) ratio within the S&P 500 is now back at the two.5x level and nearing the loftiest levels up to now 12 months. Additionally it is greater than 1 standard deviation higher than the typical over the prior 12 months as well.

Indeed, the last time the S&P 500 traded at such a lofty multiple was late July which marked a big short-term top out there as seen within the chart.

Velocity

The SPY is beginning to lose upside momentum because it stalls out on the $4600 resistance level. 9-day RSI got to overbought levels but has weakened. Bollinger Percent B approached 100 then softened. More importantly, MACD just generated a sell signal by turning negative at the same time as the S&P 500 hit an annual high.

The previous two times this occurred coincided with a pointy pullback within the S&P 500 as highlighted within the chart above. See if the identical happens once more.

VIX

The VIX made a recent annual low on Friday, closing below the important thing 12.50 level after hugging that price level for 2 weeks.

The previous two times it got to such depressed readings after prolonged consolidation coincided precisely with tops within the SPX shown below. This will once more be an opportune time to take a short-term short position within the S&P 500.

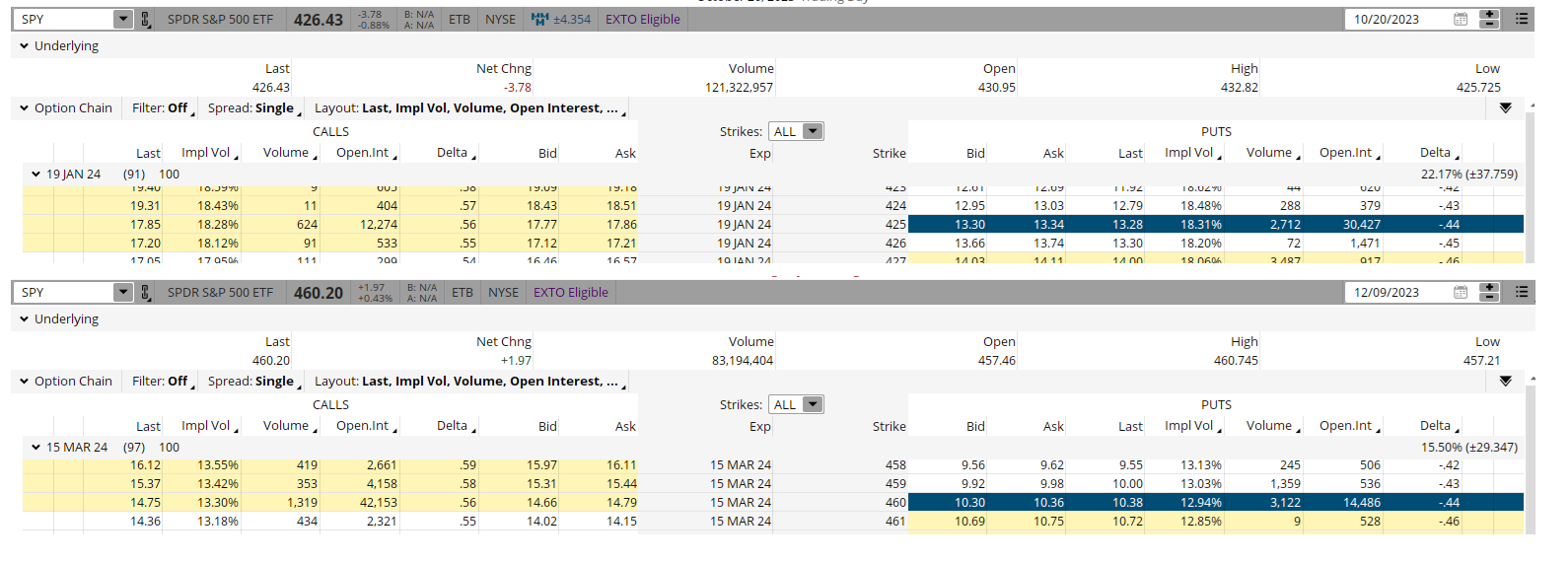

The brand new low levels of VIX also mean option prices are the most cost effective they’ve been in a 12 months. A comparison of put prices from October 20 (when S&P 500 was near the lows) versus Friday’s close with SPY at highs shows just how less expensive.

On October 20, the SPY closed at $426.43. The marginally out-of-money $425 put ($1.43 out-of-the-money) was trading at $13.32 and had 91 days to expiration (DTE). Implied volatility (IV) was over 18.

Friday shows that the SPY closed at $460.20. The at-the-money put (only 20 cents out-of-the money) was trading at $10.33 and had 97 DTE. Implied volatility was just below 13.

So, the present at-the-money $460 put had more time to expiration (97 days versus 91 days) which should theoretically make it dearer. It was also barely less out-of-the money ($0.20 in comparison with $1.43) which should make it dearer. Plus, the SPY was higher priced by nearly 34 points which should make the value of the comparative put higher priced as well.

But, IV has been hammered to the bottom levels of the 12 months. In our example, the puts fell from over 18 to under 13 IV. This makes option prices less expensive. To put it in percentage perspective, the associated fee of the puts fell from over 3% in October to only over 2% now.

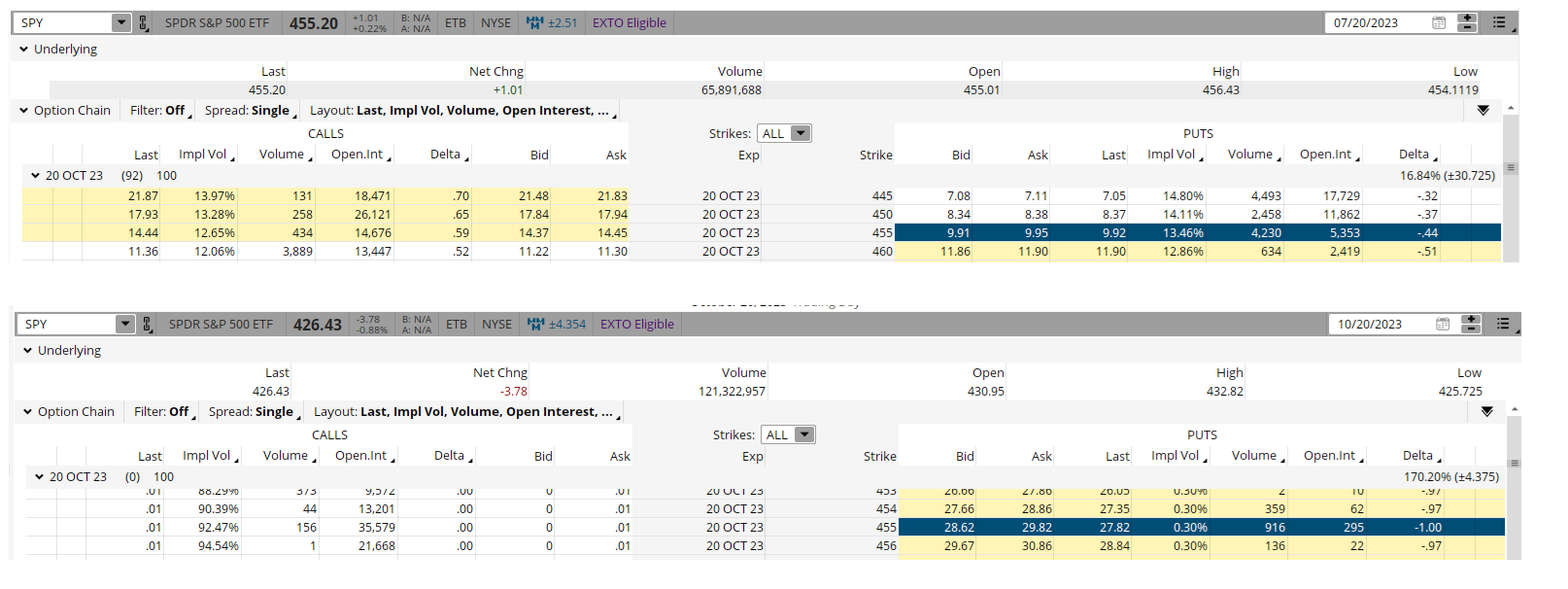

In the event you had bought the same at-the-money puts last time SPY was this almost this high and VIX was almost this this low in late July, you’ll have been rewarded very nicely as shown in the choice montages below.

The at-the-money October $455 puts with 92 DTE might have been bought for just below $10 on 7/20. These same puts closed on October expiration at just below $30. This equates to a 200% return in three months.

Actually, not all trades will work out this well and even this profitably-if profitably in any respect. That is trading in any case.

But using the POWR Options approach can put the percentages in your favor. And at the top of the day, trading is all about probability, not certainty.

POWR Options

What To Do Next?

In the event you’re on the lookout for one of the best options trades for today’s market, you need to take a look at our latest presentation Methods to Trade Options with the POWR Rankings. Here we show you consistently find the highest options trades, while minimizing risk.

If that appeals to you, and you should learn more about this powerful recent options strategy, then click below to get access to this timely investment presentation now:

Methods to Trade Options with the POWR Rankings

All of the Best!

Tim Biggam

Editor, POWR Options Newsletter

SPY shares closed at $460.20 on Friday, up $1.97 (+0.43%). Yr-to-date, SPY has gained 21.67%, versus a % rise within the benchmark S&P 500 index through the same period.

Concerning the Writer: Tim Biggam

Tim spent 13 years as Chief Options Strategist at Man Securities in Chicago, 4 years as Lead Options Strategist at ThinkorSwim and 3 years as a Market Maker for First Options in Chicago. He makes regular appearances on Bloomberg TV and is a weekly contributor to the TD Ameritrade Network “Morning Trade Live”. His overriding passion is to make the complex world of options more comprehensible and subsequently more useful to the on a regular basis trader.

Tim is the editor of the POWR Options newsletter. Learn more about Tim’s background, together with links to his most up-to-date articles.

The post Valuations, Velocity, and VIX Point To A Probabilistic Pullback In S&P 500 (SPY) appeared first on StockNews.com